I have been meddling with Alternative Finance (AltFi) since 2011. It’s endlessly fascinating. So, today I don’t want to talk about the alternative investment Equity Crowdfunding, but the alternative currency, Bitcoin.

Two years earlier, a mysterious individual or group invented the first, and even more mysterious, cryptocurrency. It was named Bitcoin. Its value, once it became live in 2010 was 0.06 US cents. It has peaked and been blown apart several times to cries of ‘bubbles’ & ‘scandal’. The value now is hovering around $4,400, on a seemingly endless march north.

So, if you had invested $1000 in April 2011, just as a punt, when the price was $0.7, that $1000 would now be worth over $5m. You might be very sorry to have passed up on that one. More realistically, you might have invested in 2012 at a value of around $10/20 - you would still be smiling.

The story goes that the first use of a Bitcoin was recorded on 22nd May 2010, when a Bitcoin enthusiast posted that he wanted to buy two large pizzas for 10,000 Bitcoin, just to get things started. Another enthusiast agreed, bought the pizzas for $25/£19 and delivered them, receiving 10,000 Bitcoin. At today’s exchange, the two pizzas cost around $40m/£30m. This event is still celebrated by the community as Bitcoin Pizza Day. The guys have a sense of humour.

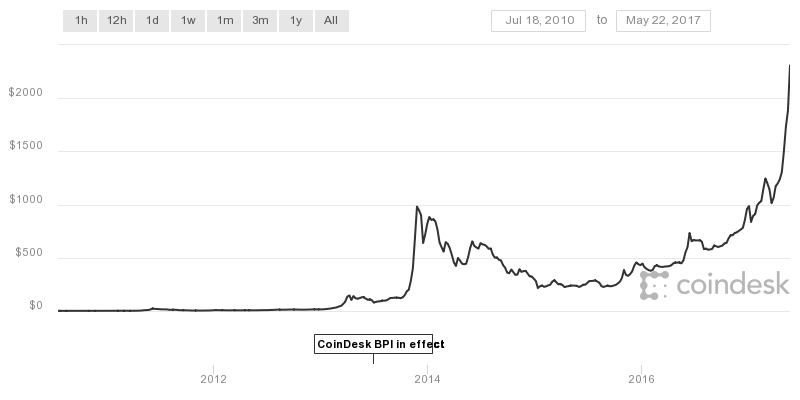

Below is the price chart as supplied by Coindesk – note that the final price of just over $2,000 is recorded in May 2017. That price, considered bubblematic in the extreme at the time, has now topped $4,600 recently.

Credit: Coindesk

So, what does that, and yet is still very much not mainstream? What is driving this crazy surge in value and can it be maintained? Actually, what the hell is Bitcoin anyway?

Here we will look at the early days and its development and then in the next post we will look at what is happening now and in the future. It’s some ride and, if you haven’t joined by now, you may just be too late.

In the original paper drafted by the group or individual who created Bitcoin, it states that the idea behind it is to create a frictionless method of money transfer without using any institutional group, such as banks, etc. It was open source, available to all. So how did they, he or she attempt this?

It’s complicated. But a quick explanation follows – this is not meant to be a definitive explanation so, if you know your Bitcoin, skip this bit.

Bitcoin uses the power of computers and the internet to create a very effective network of computers. It couldn’t exist in a pre-2000 world. This community creates a virtual currency which exists only as code or hashes and can be dealt only via the very secure Bitcoin Blockchain. The Blockchain is a ledger of all Bitcoin activity, controlled by the original 2008 protocol, the developers who have helped to develop it since and the users of Bitcoin – i.e. it has no one controller, no central bank. There is no need for lender of last resort as the money involved, whilst virtual, is real in the sense that neither banks nor governments or anyone can artificially create it. Actually, the term money, with its old connotations is, here, very misleading. Bitcoin is a secure exchange system operating online via its members’ computing power. The amount of Bitcoin available, and its value, are functions of the original protocol and the pure market forces of supply and demand.

Each user has a key code which is their access to their store of Bitcoin – this is issued by Bitcoin using an algorithm or hash. The key code is recognised by the system and can be viewed openly but is anonymous to everyone but the key holder. In order for the user to access their Bitcoin, they must enter the key. Once accessed, a transaction can take place. This transaction is then broadcast to the Bitcoin community, or rather, its banks of computers. At this stage, the power of the Bitcoin verification systems kicks in. Individuals (anyone registered to “mine” can play) and vast warehouses full of computing power, both known as miners, take the transaction and put it into a block – which is simply 10 minutes of Bitcoin transactions. The miners then run this encrypted information through a hash or algorithm. Bitcoin uses an algorithm called SHA-256 to create these hashes. This produces a 64 character hash that is as secure as anything we currently have on the planet.

The miners then use their computing power to work through millions of calculations to find the correct number of zeros that get added to the 10 minute block’s label. Remember, that to anyone looking at this hash, it is just a string of 64 meaningless characters – it isn’t possible to work it out backwards to the original. The number of zeros required is part of the protocol set up in the original 2008 paper. Progressively, as Bitcoin heads for its final 21m issued coin total, the number of zeros increases, making mining more difficult and more expensive. Once a miner has found this answer, it is sent to the whole network who must vote on it with 51% majority passing the block – known as the ‘proof of work’. Of course, none of this really involves people – it’s all run by computer power. This is then added to the blockchain. And so on. Originally, the process was almost immediate, but rising volumes have brought with them some time lag issues which we will look at next time.

The encryption is as close to 100% secure as we can get. The miners get rewarded with Bitcoin. Each block of the blockchain contains a record of all the transactions that have ever taken place using Bitcoin. So it is impossible to forge and each transaction can be traced forever, but with the owner of the coin anonymous.

One offshoot of this security is that if you lose your key, then you will lose your Bitcoin. There are numerous stories out there, but my favourite is the IT worker in Newport who threw out his hard drive, only to realise that he had stored his key on it. Several millions now sit under many tonnes of landfill. I would have written it down somewhere, but then that rather goes against the whole Bitcoin ethos…

An interesting aspect of the loss of Bitcoins is the number involved. Around 25% of the Bitcoin mined so far have been lost. In the early days, it seems Satoshi, him/her or themselves, mined many of the coins themselves – a way of kickstarting the project. An estimate has put this figure at 1m coins. None of these have since been traded. So, for what was then around $30k (at $0.03), the real Satoshi would now own (at $4,000) $4,000,000,000. The assumption goes that if none of this has been cashed in for profit, then all of it must be lost. It hasn’t been destroyed or spent as this would have left a record. We will probably never know.

One major flaw in Bitcoin, which will probably never be worked out, is its openness to criminal use. So secure and so anonymous is the system, that it suits criminal activity almost perfectly: it’s just an unfortunate consequence of its brilliance.

Silk Road is the classic tale. By using both TOR (the Dark Web) - ironically set up and still used by the US Navy - and Bitcoin, Silk Road established itself as the platform for anything criminal and untraceable. It was simple – buy or sell drugs, guns or, in the end, whatever you liked, and it was secure via TOR and payment was untraceable with Bitcoin. Set up by a double graduate, Ross Ulbricht, it soon became one of the largest and fastest growing internet companies on the planet. The FBI and the world knew about it but couldn’t do anything as they couldn’t find Ulbricht, or rather, didn’t know who he was, and couldn’t trace the platform HQ. In the end, Ulbricht had made one mistake, he had used his real name and address on a blog site in the early days and, although he had erased this, a copy still existed on the web. The FBI managed to find this and locate him. They then had to catch him online on Silk Road acting as the owner. This they did and he is now in prison serving two life sentences without parole. As with most Bitcoin scandals, it seems the perpetrator was touching madness, flying way too close to the sun and got burnt. Some of his last rants online come straight from Colonel Walter E Kurtz. And whilst its use by criminals is a problem for the mainstream, it doesn’t mean it should be written off. It is unfortunate that this aspect of Bitcoin has become possibly its most infamous, outside of the believers’ circle.

This, however, may be changing, as we shall find out in the next post - what’s happened to Bitcoin and what might its future hold?